In advance of our event at the Bank of England on 21 March 2017, we asked interested parties to write on the theme: Worthy of trust? Law, ethics and culture in banking…

This short opinion piece is based on a longer article we published last year in the European Journal of Finance, ‘Changing the Culture of Finance: Regulation, Self-Regulation and Corporate Governance’

Three years ago we edited a book called Capital Failure: Rebuilding Trust in Financial Services (Morris and Vines, 2014), which included contributions from philosophers, lawyers, historians and industry practitioners. All of the authors of that book share our belief that firms in the financial services industry need to behave in a more trustworthy manner.

We believe this principally because trust is important to almost all commercial transactions, because contracts are mostly incomplete in some way or other, especially when – as often happens in finance – one party has more information and expertise than the other. But trust is especially important in finance because so many financial transactions last for a great number of years. Those who save often do so for many years – for example for their pensions – and many investments only pay off a long time into the future. As a result there needs to be a continuing relationship of trust between those who save and invest, and those who provide the services of financial intermediation which connect them.

In Capital Failure we explored in some detail what makes people behave in an untrustworthy manner. Commercial arrangements necessarily involve seeking a financial return, without which there would be insufficient incentive to participate or – indeed – an ability to be helpful to others. But inappropriate exploitation of superior knowledge or monopoly power can easily end up meaning that returns are apportioned between the parties in an unfair, and unsustainable, manner. This clearly has damaging effects on the individuals who have saved and invested, on the reputations of the firms who provide the financial intermediation, and on the outcomes for society as a whole. The challenge is to ensure an outcome in which such bad behaviour does not eventuate, in the ways that it clearly did in the years running up to global financial crisis, and in the many ways which have continued to become evident since then.

In our work for the Capital Failure book, and in our subsequent investigations, we have tried to draw conclusions about the best way forward. In very broad terms we have learned that reliance on markets, coupled with light-handed regulation, is an ineffective way of encouraging trustworthy behaviour. But so too is resort to heavy-handed, imposed, regulation: firms usually find a way of arbitraging around such regulation. As a result, it is clear that some form of self-regulation by the firms themselves is an essential part of the solution. This needs co-ordination, encouragement and guidance.

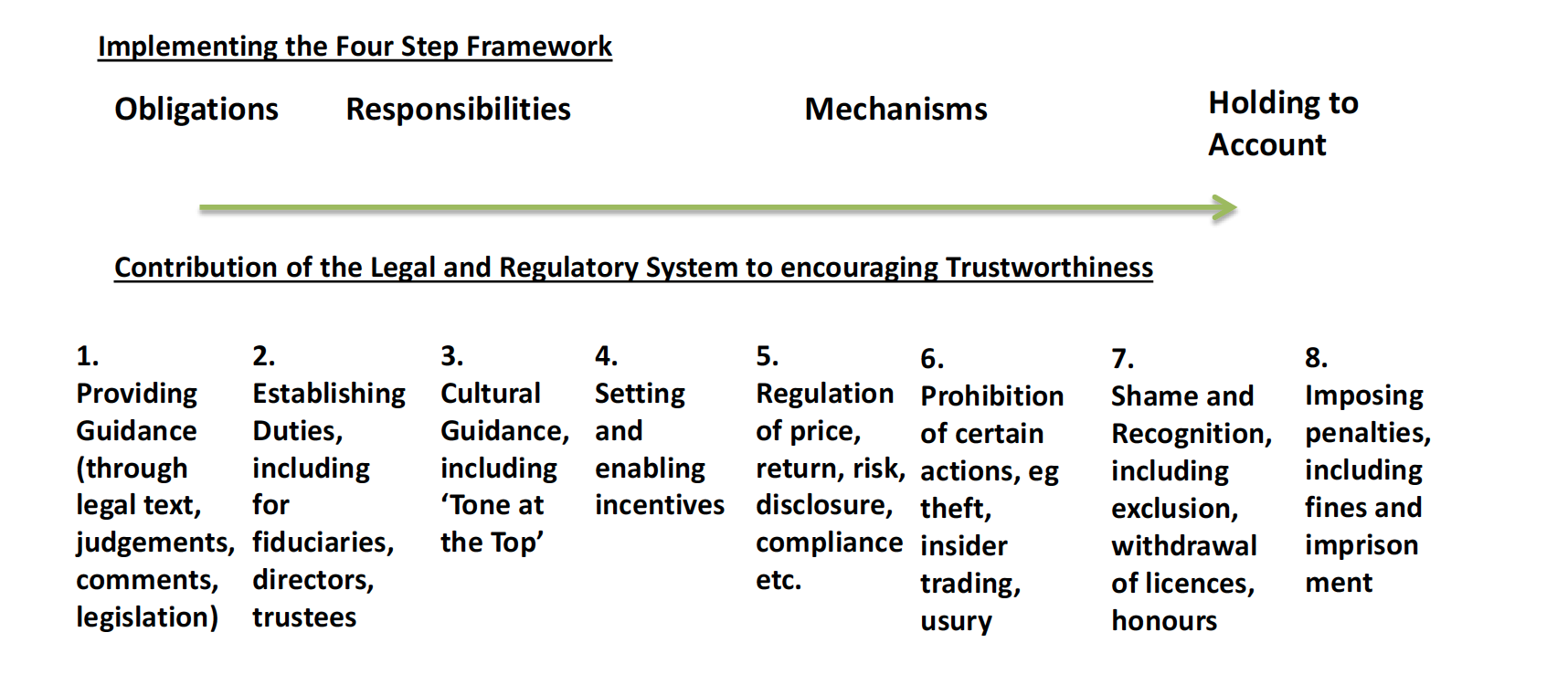

In Capital Failure we developed a four-part framework intended to provide such guidance to regulators, to policymakers and to the industry itself. We think the following components are essential:

- an appropriate specification of obligations;

- an identification of corresponding responsibilities;

- the creation of mechanisms by which these responsibilities can be carried out; and

- the holding to account of those involved, in an appropriate manner.

Who should do what is the key question which this framework can help us to understand. How much can the industry do for itself – by changing its own culture – and how much needs to be imposed by regulatory enforcement? Effective self-regulation is the ideal, both at the level of the firm and the industry, but is unlikely to be completely adequate. Regulatory control and guidance, and legal restraint and sanctions will always remain important.

It is helpful to use the following spectrum to think about how the legal and regulatory system might best contribute.

This who-should-do-what question raises challenges at all levels: for the legal and regulatory system, for the self-regulatory process, for the corporate governance of individual firms, and for the individuals who work for these firms.

It is apparent that the legal and regulatory system has several roles to play in encouraging trustworthy behaviour. It is clearly important that the legal system provide an ever-present threat of punishment for those who step over the line and behave in an unacceptable manner. But the legal system also has a broader role to play. In their judgements, judges are able to make clear the norms of behaviour which are expected of market participants. And some legal activity consists explicitly of the writing of rules, and the development of standards, which the regulatory system can then enforce. These additional roles are crucial, and they extend much further than many intelligent commentators have previously realised.

Nicholas Morris and David Vines

{kind=link}